EE#22 Private finance to the rescue

It’s Budget Week, and no you don’t want policy certainty.

Budget is the optimal word. As Jeremy Hunt and Rachel Reeves like to remind us, there is not much money around. Now, fiscal constraints come from political decisions rather than immovable economic ones, but as neither economic nor public opinion evidence has convinced either party that there is room to borrow, we must live within them.

The problem with that is that the UK’s capital investment requirements aren’t going anywhere. The National Infrastructure Commission points to £28bn a year in transport alone in the next parliament. The annual NHS maintenance backlog is now over £4bn a year, and that’s before the backloaded New Hospitals Programme. The CCC’s £50bn estimate of the cost of decarbonisation is in 2019 prices and doesn’t account for underinvestment since then. If public investment is out that means we are back to unlocking the wall of private finance to try and solve these problems.

The CCC is clear that the ‘vast majority’ of net zero capital at least will be private. The issue we have is that 1) the private sector doesn’t like to lead, which means higher public spending initially, and 2) the public-private split varies across sectors. Nature restoration, as a clear public good, will require more public to private than EVs where the state’s role is ensuring fairness.

The private sector is not helping itself. Step into any meeting and ad nauseam they will tell you we just want consistency! Parking that is literally the financial sector’s job to profit from risk, it’s also not true. If your concern is things aren’t working then clearly something must change. Calling for consistency has only convinced Labour to stick to Tory spending plans, plans which do nothing for the underlying capital constraints the private sector would like to see improved.

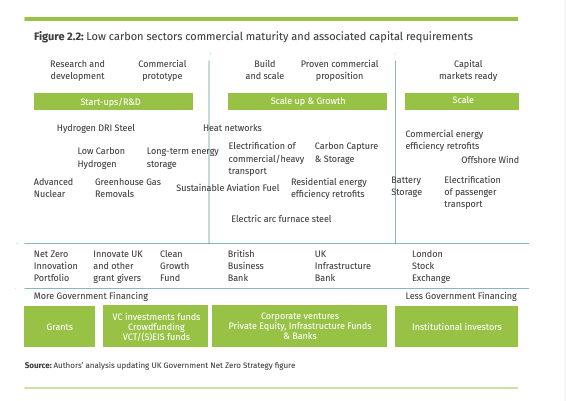

So what do we do instead? The reason the financial sector is not financing say green hydrogen or sustainable agriculture is not because of some arcane financial sector regulation, it’s because those markets are not yet viable for anyone but the riskiest investors (see below). Improving investment is a real economy challenge, not a financial sector one.

Green finance regulation is hamstrung by government dragging its feet. At COP26 Sunak announced a host of important interventions including mandatory transition plan reporting (how firms will move to net zero) and the green taxonomy (a bible of what is legitimate to call a green investment). But neither has come to fruition and other countries have overtaken us. That has raised the cost of doing business. The UK should’ve set the standards abroad now we have divergence.

Delay also leaves ambitious financial firms out on a limb, without legal and regulatory backing it’s easier for firms to backtrack on climate promises (especially under political pressure in the US) - one of the reasons Blackrock and JP Morgan recently left the CA100+.

We need to shift from thinking about finance in its own right and instead as part of an explicit industrial strategy. The private sector doesn’t care where it makes its money, it’s political parties that do. You can only work out the how and where of investment if you know the why. If the goal is net zero, then your question is not ‘How do we get the private sector to invest (because the state won’t)’, but ‘How do we direct private finance to the highest emitting sectors’?

We have done this before. A decade ago the state wanted to reform the electricity market to encourage more renewable energy and reduce emissions. It did not start with the investment question it started with the problem. Very quickly it became clear that the high capital cost of offshore wind was the barrier to reform.

The state didn’t solve that alone. The first step as always with industrial strategy was to socialise government and the private sector around the specific problems. There were regulatory issues - finding and permitting sites was hard and expensive. Supply chain issues - ports lacked capacity. There were financial issues, lots of upfront money but no guaranteed returns. Through various groups, the state and the sector tackled each of these in turn. The Green Investment Bank provided capital (and refinancing), while the Renewables Obligation and later CfDs made revenues predictable.

There are clear lessons here for financing the next wave of green sectors. The first is that you can’t do anything without a strategy or partnership. With no strategy, decisions to say become a world leader in green hydrogen, end up being politically vulnerable and risky. We can’t define what success looks like and other parties may take a different view.

The second is that state investment is vital, but only when you’ve defined the specific problems it needs to solve. Just promising state money without working out why or where helps no one. We should always pair investment with wider reforms to maximise every pound.

Third is that you will never remove risk entirely. The point of partnership is not just to decide on actions, but to be able to warn, discuss or explain when a change of direction is happening. The private sector hated Sunak’s walkback on EVs and heat pumps because they didn’t know it was coming and didn’t know why.

None of that is going to come from this budget. But if we want future budgets to tackle emissions we need to be a lot clearer on what investment is required where, and why.